A market structure where there exists just one seller of a particular good. This market structure is the opposite of a perfectly competitive market.

The assumptions that are required for a monopoly to hold are as follows:

- A single firm controls the output of the entire industry - this ensures that this firm is a price maker and sets the price that maximises their profits.

- There are significant barriers to entry - the presence of these barriers ensures that the monopoly power of the firm is protected, as no other firm can enter the industry.

If a firm operates in an industry where these conditions are met it creates a monopoly market structure. However, a monopoly is more of a theoretical market structure as there are very few practical examples of one firm controlling an entire market (pure monopoly). Often the theory of a monopoly is important to assess the impact of one large firm dominating several small firms.

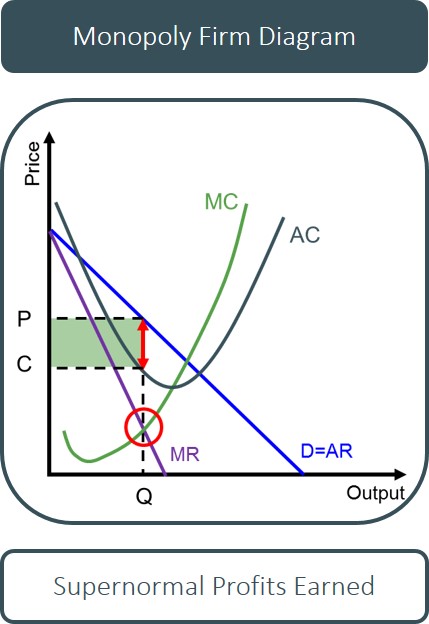

Just like under monopolistic competition, the monopolist faces a downward sloping demand curve (AR) as they are the only seller in this particular market, rather than the perfectly elastic demand curve under perfect competition. However, in the case of the monopolist, this is also the market demand curve as this is the only firm supplying this type of product to the market. It is this unique feature in monopoly markets that grants the monopolist a large degree of monopoly power. The monopolist profit maximises at the point where MR=MC, but because of the significant monopoly power, the price that they charge is represented by the price they can set according to the demand curve for that specific quantity of goods. The monopolist can do this because the monopoly power makes them a price maker. Because of the fact that the AR curve is higher than the AC curve for the monopolist at this point, it creates the conditions for the monopolist to extract supernormal profits from the market. In the long-run the monopolist outcome is unchanged as the presence of significant barriers to entry prevent new competitors from joining the market and stealing the supernormal profits available.

It is important to consider that this outcome is all based on the assumption that there exists significant barriers to entry in the market for the situation of supernormal profits to hold in the long-run.

However, the level of supernormal profits a monopolist receives will be subject to changes in market conditions such as the level of demand for the good. For instance, monopolists are price makers and therefore set their own prices and the demand curve determines how much output will be sold on the market at that price. A monopolist does not have the ability to set both the price and quantity of output. If the demand curve shifts inwards or the average costs of production for a firm increase, then this will reduce the level of supernormal profits belonging to the monopolist. If market conditions go against that of a monopolist and causes the firm to make economic losses in the short-run, then in the long-run the firm will leave the market and as the firm is the only firm in the market, the market will cease to exist in the long-run. This means that monopolists have to adhere to the standard shut-down points of all other firms.

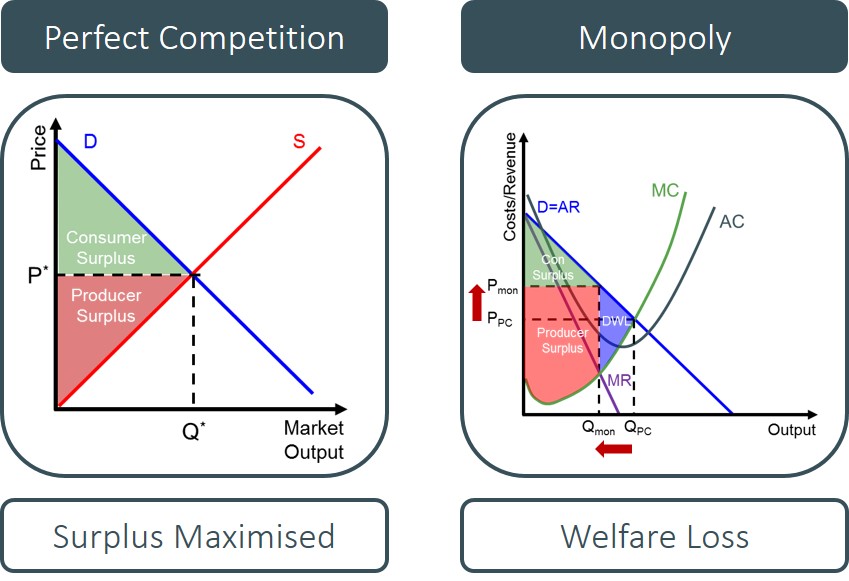

An interesting analytical point to raise when talking about monopolies is the comparison against a perfectly competitive market structure. This is because a monopoly is at the opposite end of the market structure spectrum when compared to perfect competition. When compared to this market structure the market equilibrium is more inefficient and results in lower welfare than compared to a perfectly competitive market because of the fact that monopolists are price makers. The optimal output level for monopolists is below that of a perfectly competitive market, as they set a higher price to maximise profits. As a result, this means that producer surplus increases because of the higher price and consumer surplus decreases due to the higher price. However, as the loss of consumer surplus is larger than the gain in producer surplus, there is an overall dead weight loss triangle created. Under a perfectly competitive market, social welfare is maximised as a result of producing at the point of allocative efficiency. Therefore monopolists reduce the overall level of social welfare in the economy, which is often why they are perceived as bad for an industry.

In terms of efficiency, monopolies are both allocatively and productively inefficient. It is productively inefficient because the monopolist does not produce at the minimum of the average cost curve. This is because the monopolist profit maximises and that production point corresponds to an average cost that is above the minimum, resulting in productive inefficiency. As for allocative efficiency, the monopolist has significant monopoly power, so it sets a price above the marginal cost and the allocative efficiency condition of P=MC is not met.

However, the question over whether a monopoly leads to dynamic efficiency is uncertain. The answer to this question identifies whether a monopoly market structure is better or worse than perfect competition and this is the key evaluation point to mention regarding monopolies. The reason for the uncertainty, is it all depends on what type of industry the monopolist operates in (the scope and importance of innovation and invention in the market) and whether dynamic efficiency can be easily achieved and whether from the monopolists perspective it is rewarding to invest and innovate.

For instance, the monopolist may be more dynamically efficient than perfectly competitive markets, if the monopolist uses the supernormal profits made in the short and long-run to invest research and development projects. By doing so, this will encourage innovation and invention into the production process, create X-efficiencies and improve the productively efficient point for the firm. In terms of the impact on a modern developed economy, if sustained it will increase the productive capacity of the economy and may even encourage other firms to become more dynamically efficient. This is most likely to be the case in industries where innovation and invention is required to continue to yield profitable results for the monopolist i.e. technology driven industries such as the upcoming driver less car market.

However, there is a fear that monopolists may be encouraged reap the supernormal profits made and without the fear of new competition coming in, divert those profits as dividends to investors and shareholders, increasing the shareholder return on the company instead of investing in research and development projects. The monopolist can do this because of the presence of significant barriers to entry. If this is the case then the market becomes dynamically inefficient and the outcome is worse than perfect competition. This occurs in industries where the rewards for innovation and invention are minimal e.g. service providers such as barber shops.

Despite all these problems with a monopolist, there may well be an advantageous case for one firm to control the entire infrastructure of an industry, as some markets involve significant initial infrastructure costs which would be unnecessary to duplicate. Therefore, to avoid these costs it is beneficial for the market to become a monopoly. This allows the monopolist to take advantage of the large economies of scale present, than have lots of smaller firms inefficiently compete over the market, raising costs and prices in the process. This is an example of a natural monopoly.