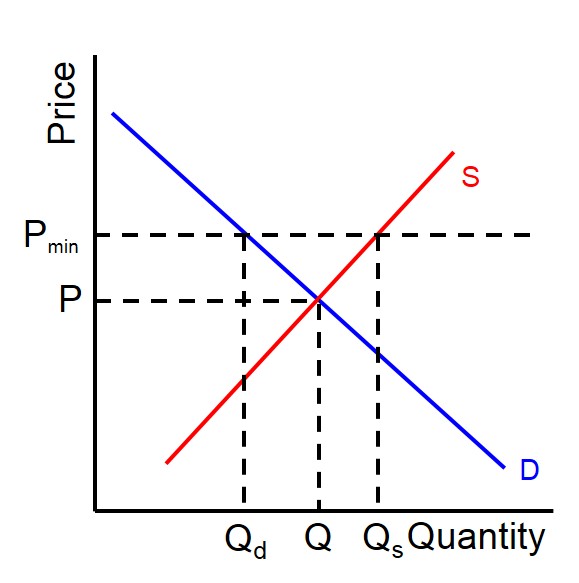

A scheme imposed by Government regulation which prevents prices falling below a certain level. Minimum prices are normally set at a level above current equilibrium price.

Below is an example of a minimum price implaced in a market successfully. In this instance the minimum price creates an artificial excess supply as producers have a greater incentive to produce more at a higher price but consumers wish to consume less and switch to cheaper alternatives. But this only occurs if the minimum price is placed above the prevailing market price as shown below. If it is placed below the current market price then it would have a neglible effect on the market.