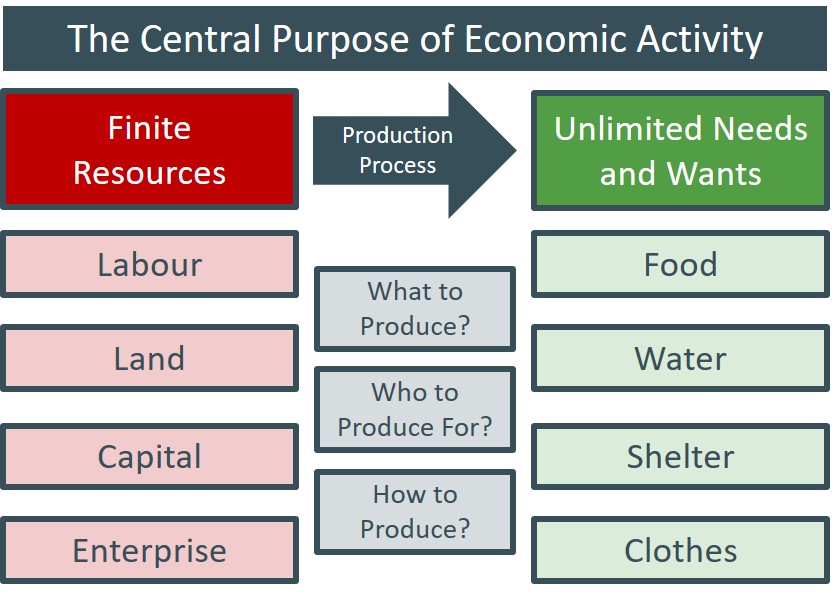

Is one of the fundamental economic theoretical principles in the operation of any economy. It asserts that any economy has a limited amount of economic resources (factors of production) at its disposal and therefore producers need to identify the best way of allocating these scarce resources to best satisfy the infinite needs and wants of consumers across the economy. This all runs on the basis that consumers tastes and preferences are ever-changing and producers need to find the best way of diverting a finite amount of resources to the goods and services which hold the greatest value and importance to consumers. Therefore, the economic problem is driven by two concepts; choice, and scarcity. Producers have to make tough choices by prioritising the human wants that can be fulfilled alongside what is feasible for them to produce given those scarce resources. Each choice represents an opportunity cost for producers due to the scarcity of these resources. The ability of producers to achieve the optimal allocation of resources can be best represented by looking at the PPF of any economy.