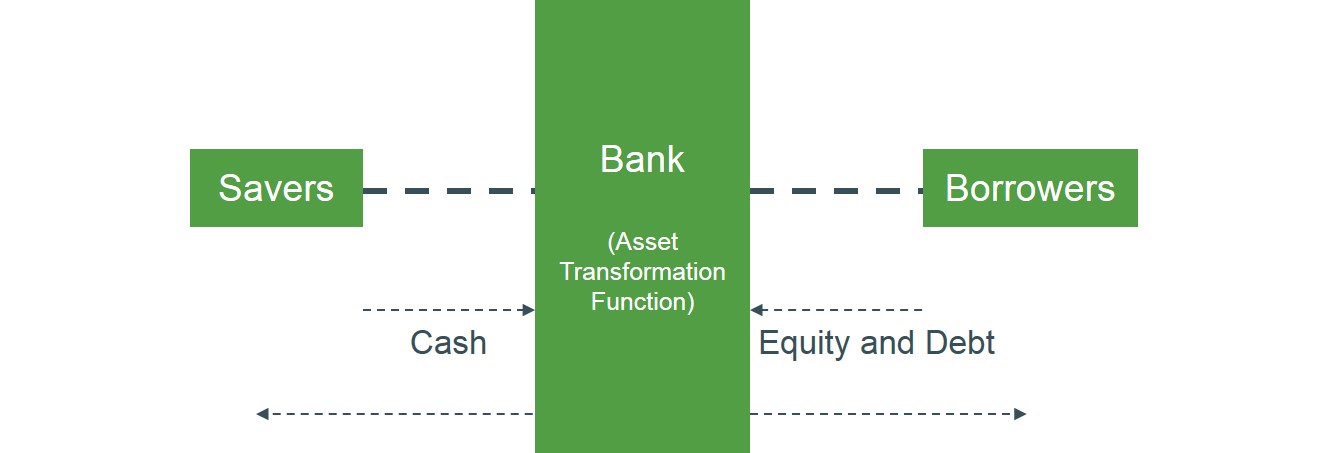

The process in which banks convert large quantities of short-term, low risk, small and liquid deposits into a small number of much larger, long-term, riskier and illiquid advances (loans). This is how individual banks make majority of their profits by transforming assets to meet the incompatible needs and wants of borrowers and lenders simultaneously.

The main risk with this type of approach for banks, is if a large long term loan is funded by a large number of small short term deposits, the bank may experience problems meeting the demands of depositors if large numbers decide to withdraw their deposit. In this situation the mismatch between the terms of depositors and borrowers is problematic as the loans may not be redeemable in the short term and this creates liquidity issues i.e. there may not be enough cash immediately available to allow depositors to withdraw their savings.

The diagram below illustrates how banks take cash from savers (surplus units - total income exceeds total expenditure) and the bank issues it off to borrowers (deficit units - total income exceeded by total expenditure) through loans in exchange for their debt (to be paid back at a later date).