Money that has been invested, in contrast to debt capital, which is not repaid to the investors within a fixed period of time. The fund provider instead receives a percentage of the ownership as well as future company profits. These funds can then be used to act as a buffer stock to absorb any losses companies or banks make.

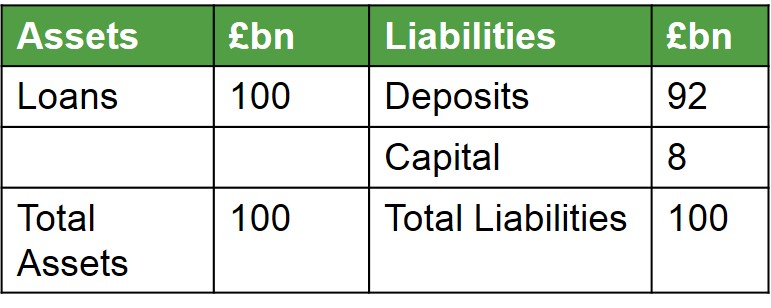

Below is an example of a balance sheet for a bank and the role that capital can play in a bank. In this instance the bank has £8bn worth of capital to absorb any losses that bank may make specifically concerning non-performing loans. So as long as the bank can maintain their losses below £8bn it will always remain in a solvent position on the balance sheet - this is the main objective for many banks to ensure confidence in the bank from customers and regulators. However, if the losses exceed £8bn then the bank does not have capital to neutralise the losses and therefore becomes insolvent i.e. liabilities outstrip assets.